You want to provide for your child. It’s a fundamental instinct that shapes so many decisions you make, from choosing a neighborhood to selecting the right school. You work hard to build a legacy, hoping that the property and money you accumulate will provide a safety net long after you’re gone. When you decide to begin setting up a trust fund for your child, you’re making a profound commitment to their well-being. However, creating a trust for a child involves more moving parts than most parents expect. It’s easy to feel overwhelmed by legal terminology, the structure of the trust agreement, or questions about how the trustee will manage what you leave behind. Many parents begin this process with the best intentions, only to make avoidable mistakes that complicate trust administration or reduce what ultimately reaches their child. These issues tend to show up again and again among loving and careful families. By looking closely at the biggest mistakes parents make, beginning with selecting the wrong trustee, you can build a plan that protects your child’s future and reflects the legacy you want to leave.

Mistake No. 1: Selecting the Wrong Trustee

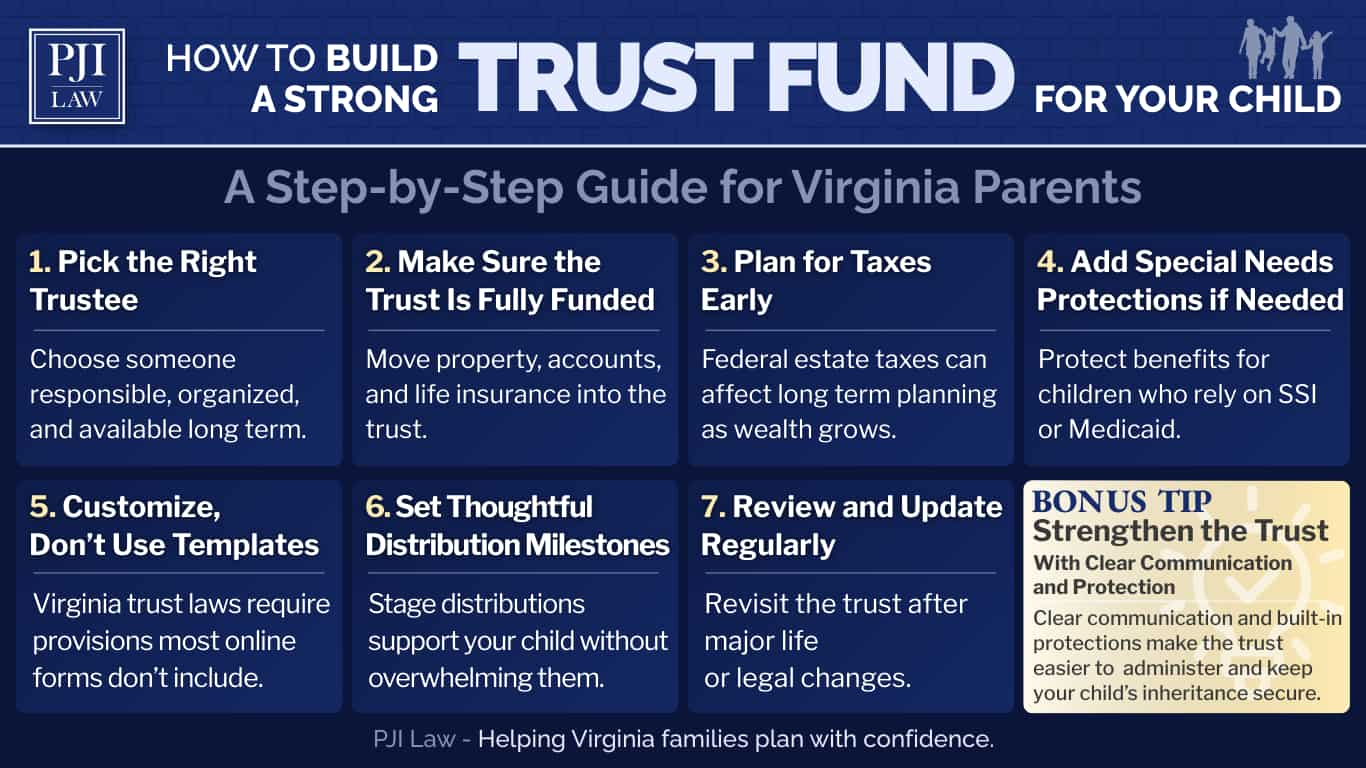

One of the most common mistakes parents make when setting up a trust fund for a child is choosing the wrong trustee. It’s natural to think of a close friend or family member first. You may trust them personally, but that doesn’t always mean they have the financial judgment, recordkeeping skills, or long-term availability needed to manage a trust.

What Parents Often Overlook When Choosing a Trustee

The trustee’s role is significant. They’re responsible for:

- Managing the assets placed in the trust

- Following the instructions written in the document

- Keeping detailed and accurate records

- Making distribution decisions based on your child’s needs

- Staying objective even when emotions or family pressure are involved

This is more than a ceremonial title. It requires consistency, organization, and sound judgment over many years.

When a Parent Serves as Trustee

Some parents decide to serve as the initial trustee because they understand their child’s needs and have a clear sense of how they want the money managed. This can work well, especially while the child is young. But even as a trustee, a parent must meet the same fiduciary standards, including:

- Careful recordkeeping

- Strict adherence to the trust’s instructions

- Objective decision-making

It’s also important to name a reliable successor trustee who can step in when you’re no longer able to serve.

When a Professional Trustee Makes Sense

Many families eventually choose a professional trustee or corporate fiduciary, not because relatives aren’t trustworthy, but because trust administration can be demanding. A professional trustee:

- Remains neutral

- Follows the document closely

- Provides long-term continuity

- Reduces the risk of conflict among family members

This option is especially helpful when a trust is expected to last well into adulthood or support a child with lifelong needs.

Evaluating Family Members as Trustees

If you’re considering appointing a sibling or a grandparent, think carefully about whether they can:

- Make difficult decisions, including saying “no” when needed

- Resist pressure from family dynamics

- Keep accurate, consistent records

- Commit to serving for as long as the trust requires

A trustee who feels overwhelmed or unprepared may unintentionally create confusion or conflict. Evaluating the person’s skills, temperament, and long-term availability helps keep the trust running the way you intended.

Mistake No. 2: Failing to Fund the Trust Properly

Another major mistake parents make is assuming the trust fund is complete once the document is signed. In reality, a trust exists only on paper until assets are formally transferred into it. Parents often spend time creating thoughtful instructions for their child’s future, but then forget the essential step of moving property, accounts, or insurance proceeds into the trust’s name. Funding a trust requires more than good intentions. If you own a home, investment accounts, or other assets in your individual name, those assets won’t automatically flow into the trust when you pass away. They may go through probate instead, which delays access for your child and exposes your estate to a process you were trying to avoid. Common assets parents overlook include:

- Real estate deeds

- Bank accounts

- Brokerage accounts

- Life insurance policies and beneficiary designations

- Business interests

- Personal valuables or collections

Each asset has its own process for retitling or designating the trust as the beneficiary. Parents sometimes complete part of the funding but leave out key items, which leads to a patchwork plan and confusion later. In some cases, the child receives only a portion of what the parent intended because the unfunded assets weren’t covered by the trust. Funding is also important for trusts that continue into adulthood. A trust meant to support education, housing, or long-term financial growth needs resources in place from the beginning. If the trust is empty or partially funded, the trustee won’t be able to follow your instructions or meet your child’s needs the way you envisioned. Taking the time to review each asset and confirm it’s properly aligned with the trust keeps your overall plan intact and helps protect your child’s future.

Mistake No. 3: Ignoring the Impact of Estate Taxes

Many parents assume estate taxes won’t affect their family because the federal exemption is high, but this assumption can become a costly mistake when setting up a trust fund for a child. Over time, assets grow, homes increase in value, investment accounts compound, and life insurance proceeds may be larger than expected. A trust that begins modestly can eventually push an estate into taxable territory, especially over the course of twenty or thirty years.

Estate Taxes in Virginia

Virginia doesn’t impose a separate state estate tax, but families are still subject to federal rules. If your estate exceeds the federal exemption at the time of your passing, the amount above that threshold may be taxed. Parents who don’t consider these long-term financial realities sometimes learn too late that a significant portion of what they meant to leave their child will be paid to the government instead.

How Trust Structure Affects Taxes

Understanding how different trust structures work helps parents avoid surprises. For example:

- A revocable trust keeps assets in your taxable estate because you retain control

- An irrevocable trust may remove assets from your taxable estate, depending on how it’s drafted and what powers you keep

- Life insurance held outside your estate may reduce what’s taxed at death

- Gifts made during your lifetime can reduce the size of your taxable estate later

When Tax Planning Is Important

Tax planning is especially important if you:

- Expect your wealth to grow significantly

- Plan to purchase more property

- Hold large life insurance policies

- Own investment accounts likely to appreciate

- Anticipate receiving an inheritance yourself

Without a thoughtful structure, the trust fund you created for your child may shrink due to taxes that could have been avoided. Reviewing your exposure now helps keep more of your estate available for your child’s long-term needs.

Mistake No. 4: Neglecting Special Needs Provisions

Parents who have a child with a disability often make one well-intentioned but serious mistake: creating a standard trust fund without including special needs provisions. A traditional trust that works well for another child can unintentionally harm a child who relies on government assistance programs like Supplemental Security Income or Medicaid.

Parents who have a child with a disability often make one well-intentioned but serious mistake: creating a standard trust fund without including special needs provisions. A traditional trust that works well for another child can unintentionally harm a child who relies on government assistance programs like Supplemental Security Income or Medicaid.

How a Standard Trust Can Create Problems

The issue isn’t the inheritance. It’s the structure. A trust can jeopardize benefits if it:

- Gives the child control over distributions

- Requires the trustee to pay for basic support

- Allows direct access to funds meant for supplemental needs

When this happens, the state may treat the trust assets as the child’s personal resources. This can lead to the loss of essential services, including medical care, housing, and long-term support.

What a Special Needs Trust Can Provide

Virginia allows parents to create a Special Needs Trust, which is designed to supplement, not replace, government benefits. This type of trust can cover expenses such as:

- Travel

- Therapies or counseling

- Specialized medical equipment

- Technology that supports communication or mobility

- Education and recreational activities

When drafted correctly, it preserves the child’s eligibility for assistance while giving the trustee room to support the child in meaningful ways.

Why Timing Matters

Parents often assume they can add special needs language later or rely on general trust terms to cover everything. Unfortunately:

- Fixing an improperly drafted trust is sometimes difficult

- Certain errors can’t be corrected once the trust is funded

- The child may lose benefits during the correction process

A trust that lacks the right protections may leave the child with fewer resources and create stress for the family when stability matters most. Including special needs provisions from the start protects your child’s long-term security and keeps the trust aligned with their unique needs.

Mistake No. 5: Using a One-Size-Fits-All Template

Another mistake parents make is relying on a generic trust form they find online. These templates often look simple and appealing, especially when you’re trying to create a trust fund quickly. The problem is that trusts for children need to address issues that a basic template can’t cover, and Virginia has its own legal requirements that many online documents fail to meet.

Why Generic Templates Fall Short

A standard template may not include essential provisions, such as:

- Directions for how money should be managed for a minor

- Protections against future creditors

- Clear rules for when and how the trustee can make distributions

- Instructions for education expenses or healthcare support

- Guidance for staged distributions as your child grows

Without these elements, the trustee may struggle to carry out your intentions, and the trust may not function the way you expected.

Virginia Law Adds Another Layer of Complexity

Virginia’s trust laws, including the Virginia Uniform Trust Code, set specific requirements for:

- How a trust is created

- What powers the trustee has

- How beneficiaries’ rights are defined

- How the trust must be administered

A document that isn’t drafted with Virginia law in mind may be incomplete or difficult to use. Parents often don’t discover these issues until the trustee tries to administer the trust and realizes key provisions are missing or unclear.

Why Templates Don’t Work for Complex Families

Families with blended households or unique circumstances face even more challenges with generic documents. Templates rarely address situations involving:

- Stepchildren

- Children from prior relationships

- Children who need long-term financial support

- Families with multiple sets of expectations or caregivers

These situations require tailored instructions to avoid conflicts and keep the trust running smoothly. A trust fund for a child works best when it reflects your family’s situation, your child’s individual needs, and the legal requirements of the state. A customized plan helps prevent confusion later and keeps the trust aligned with what you intended.

Mistake No. 6: Setting Inappropriate Distribution Milestones

Parents often put a great deal of thought into how and when their child should receive money from a trust, but many still fall into a common trap: setting distribution ages or milestones that don’t match the child's maturity, life circumstances, or future responsibilities. It’s natural to want your child to have access to their inheritance once they become an adult, but turning over a large sum at 18 or even 21 can lead to financial decisions they aren’t prepared to make.

Problems With Single Distribution Ages

A trust fund for a child should grow with them. Relying on a single distribution age can be risky because:

- Maturity doesn’t always align with age

- Outside influences can affect spending

- Life challenges can arise unexpectedly

- A large lump sum may be overwhelming for a young adult.

Many parents assume their child will be financially responsible at a certain age, only to learn later that a one-time distribution didn’t match the child’s real needs.

Examples of Staged Distribution Plans

Staged distributions help reduce risk and provide guidance over time. Instead of giving everything at once, the trust can release funds in smaller portions tied to age or personal milestones. For example:

- A portion in the mid-20s for a first home

- Another portion later, once the child is more established

- The remainder, once they’ve reached a point of financial stability

This approach offers support while still protecting the long-term purpose of the trust.

Why Trustee Flexibility Helps

It’s also important to give the trustee some flexibility. A strict schedule may not work if your child:

- Faces a medical issue

- Has educational needs that fall outside preset ages

- Experiences changes in career or personal circumstances

Allowing the trustee to make discretionary distributions for education, healthcare, or other meaningful needs lets the trust adapt as the child grows. Parents who overlook these considerations may create a trust that limits their child at the wrong moments or hands over too much too soon. Choosing thoughtful distribution milestones helps the trust keep its purpose intact throughout your child’s life.

Mistake No. 7: Overlooking the Need for Regular Updates

Once the trust fund is created and properly funded, many parents put the documents away and don’t look at them again. Life moves quickly, and it’s easy to assume the trust will keep working as intended. But a child’s needs change over time, families grow, and assets change. A trust that isn’t reviewed regularly can become outdated and may no longer reflect your goals or your child’s circumstances.

Once the trust fund is created and properly funded, many parents put the documents away and don’t look at them again. Life moves quickly, and it’s easy to assume the trust will keep working as intended. But a child’s needs change over time, families grow, and assets change. A trust that isn’t reviewed regularly can become outdated and may no longer reflect your goals or your child’s circumstances.

Life Changes That Require an Update

Parents often forget to revise their trust after major life events, such as:

- The birth of a new child

- A marriage or divorce

- A change in guardianship intentions

- The purchase of new property

- The sale of an asset originally meant to fund the trust

- Opening new accounts that need to be titled in the trust’s name

If these updates aren’t incorporated, the trust may leave out important beneficiaries or fail to include significant assets.

Legal Changes That Affect Trusts

Trusts also need updates because the law evolves. While Virginia doesn’t revise its statutes every year, changes do occur, and federal tax rules change as well. A trust created under older legal standards may:

- Miss important protections

- Contain provisions that no longer work as intended

- Fail to take advantage of more favorable planning options

Parents sometimes don’t realize their documents are outdated until a trustee or estate planning lawyer reviews them years later.

Why a Periodic Review Helps

Reviewing the trust every few years, or after a major life event, helps:

- Keep the terms aligned with your long-term goals

- Confirm that the right assets are funding the trust

- Update your instructions as your child’s needs evolve

- Reevaluate whether your trustee selection still makes sense

The person you chose years ago may have moved, may no longer feel comfortable serving, or may not be the best fit as your child grows. Regular updates help the trust stay functional, accurate, and responsive to your family’s changing circumstances.

Bonus Tip: Strengthen the Trust With Clear Communication and Built-In Protection

Beyond the most common mistakes parents make, there are two simple steps that can make any child’s trust fund stronger and easier to administer.

Talk With Your Trustee Before They Serve

A trustee who knows what’s expected will make better decisions for your child. A brief conversation now helps them feel prepared and reduces confusion later. They should know:

- Where the trust documents are stored

- Who the family’s attorney is

- Your overall goals for the trust

- The priorities you want them to keep in mind as your child grows

Clear communication gives your trustee confidence and helps keep the trust running smoothly.

Add Protections That Shield the Inheritance

A trust fund doesn’t just provide support. It also protects what you leave. Adding the right language can help keep the trust safe from:

- Creditors

- Lawsuits

- Divorce disputes

- Future financial trouble

One of the strongest tools under Virginia law is a spendthrift provision, which limits a beneficiary’s ability to transfer their interest in the trust and prevents most creditors from reaching the assets. Giving the trustee discretion over distributions also keeps the assets inside the trust, where they remain protected for your child’s future needs. These small steps add strength and stability to the trust and help preserve the purpose behind your planning.

Moving Forward with Confidence

Creating a trust fund for your child is one of the most meaningful steps you can take to support their future. It’s natural to want your plan to be simple and straightforward, but the choices you make during the process can shape how well the trust works years from now. By avoiding the common mistakes that many parents face, you give your child a solid foundation and a structure that supports them through each stage of life. Thoughtful trustee selection, proper funding, tailored provisions, and regular updates all play a role in keeping the trust aligned with your goals. Taking time to communicate with the trustee, considering long-term protections, and customizing the document to your family’s needs allows the trust to function the way you intended. These small decisions can make a significant difference in how smoothly the trust operates later. A trust fund isn’t just a financial tool. It’s an expression of your care, your values, and your hopes for your child’s future. When it’s created with attention and precision, it becomes a lasting part of the legacy you want to leave.

Build a Trust Fund That Truly Protects Your Child’s Future

We understand how much thought goes into protecting your child’s future. At PJI Law, our trust fund lawyers work closely with parents who want to set up a trust fund for their child that reflects their values and supports the child through each stage of life. If you’ve been searching online for a “trust fund attorney near me,” our team is here to provide guidance that’s personal, clear, and grounded in Virginia law. We work with parents like you across Fairfax and Northern Virginia, taking time to understand your goals and create a trust fund that fits your family’s needs. Whether you're creating your first trust fund or updating an existing plan, we guide you through each step so your child is protected today and in the years ahead. If you’re ready to create a trust fund that supports your child and reflects the legacy you want to leave, call PJI Law at (703) 865-6100 or contact us online to schedule a complimentary and confidential consultation. At PJI Law, you’ll receive white glove service and personal attention from a team that treats you like family. Copyright © 2026. PJI Law, PLC. All rights reserved.

Copyright © 2026. PJI Law, PLC. All rights reserved.

The information in this blog post (“post”) is provided for general informational purposes only and may not reflect the current law in your jurisdiction. No information in this post should be construed as legal advice from the individual author or the law firm, nor is it intended to be a substitute for legal counsel on any subject matter. No reader of this post should act or refrain from acting based on any information included in or accessible through this post without seeking the appropriate legal or other professional advice on the particular facts and circumstances at issue from a lawyer licensed in the recipient’s state, country, or other appropriate licensing jurisdiction.

3900 Jermantown Road, 2nd Floor

Fairfax, VA 22030

(703) 546-9674

https://www.pjilaw.com

Tell Us Your Situation

No cost, no obligation. We respond the same business day.

More Legal Insights

Protecting Virginia individuals, families, and businesses with personalized, attentive, and dedicated service.

Contact Info

Our Estate Planning Lawyers Office Location In Fairfax, VA

© Copyrights 2026. PJI Law, PLC. All Rights Reserved.

You should consult an attorney for advice regarding your individual situation. Contacting us does not create an attorney-client relationship.